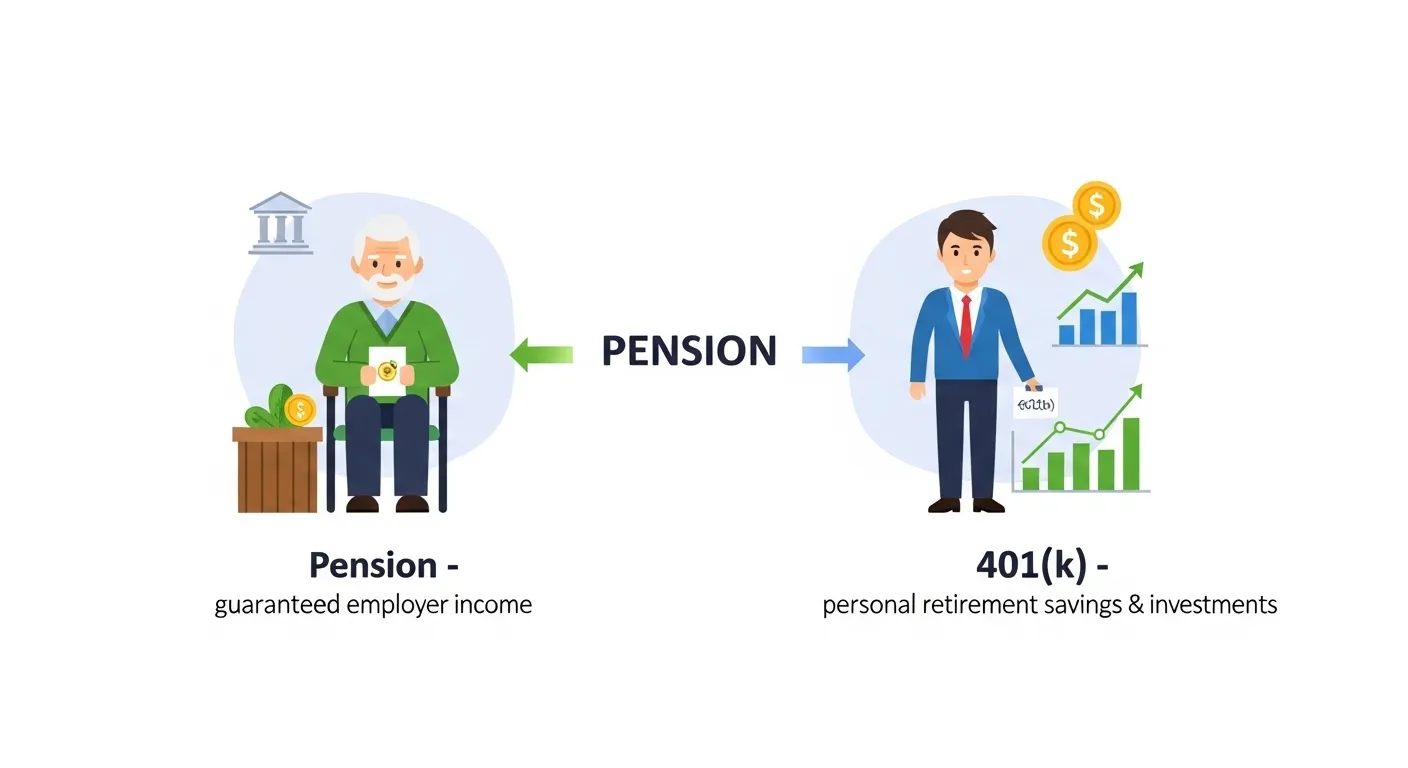

A pension is a guaranteed retirement income paid by an employer, while a 401(k) is a personal retirement savings plan where you invest your own money (often with employer contributions). 💰

Many people get confused when planning retirement because they don’t fully understand the difference between pension and 401k. This confusion is very common, especially among employees in the US and global job markets where retirement systems vary widely.

When someone hears terms like pension plan or 401k account, it often feels complicated, but in reality, the difference between pension and 401k is based on who manages the money and how retirement income is generated.

In simple words, both pension and 401k are retirement savings systems, but they work in completely different ways. That’s why users often search on Google: what is pension, what is 401k, and how are they different. Understanding the difference between pension and 401k helps you make better financial decisions for your future.

In this guide, you will learn how both systems work, their pros and cons, real-life examples, and which one might be better depending on your job or country.

Let’s break down the difference between pension and 401k in the simplest way possible.

Difference Between Pension and 401k

A pension is a retirement plan where your employer guarantees monthly income after retirement. A 401k is a personal retirement savings account where you invest your own money for future use.

👉 Example:

- Pension = fixed monthly income after retirement

- 401k = savings account that depends on investments

Definition of Pension and 401k

- Pension: A retirement plan funded mainly by the employer that provides a fixed income after retirement.

- 401k: A retirement savings plan where employees contribute part of their salary and invest it for future growth.

✔ Pension = employer guaranteed income

✔ 401k = employee-controlled investment account

Pronunciation

Understanding pronunciation helps in financial discussions and job environments:

- Pension → /ˈpen.ʃən/ (PEN-shun)

- 401k → “four-oh-one-kay”

These terms are widely used in Google Finance searches, LinkedIn job discussions, Meta career groups, and YouTube financial education channels.

Comparison: Pension vs 401k

| Feature | Pension | 401k | Similarity |

| Control | Employer manages | Employee manages | Both retirement plans |

| Income type | Fixed monthly income | Investment-based income | Both provide retirement funds |

| Risk level | Low risk | Market risk involved | Both long-term savings |

| Contribution | Employer funded | Employee + employer | Both involve savings |

| Security | Guaranteed payout | Not guaranteed | Both depend on employment |

| Flexibility | Less flexible | Highly flexible | Both for retirement |

| Growth | Fixed growth | Market-based growth | Both aim for retirement security |

👉 This table clearly shows the difference between pension and 401k for quick understanding.

Key Differences Explained Between Pension and 401k

1. Who Controls the Money

- Pension is fully managed by employer

- 401k is controlled by employee

✔ Example: company decides pension payout

2. Risk Factor

- Pension has low financial risk

- 401k depends on market performance

✔ Example: stock market affects 401k

3. Income Stability

- Pension gives fixed monthly income

- 401k income varies

✔ Example: pension = predictable paycheck

4. Investment Responsibility

- Pension requires no investment knowledge

- 401k requires personal investment decisions

✔ Example: choosing funds in 401k

5. Job Dependency

- Pension depends on employer stability

- 401k stays with employee even after job change

✔ Example: switching companies

6. Retirement Planning Style

- Pension = passive retirement planning

- 401k = active financial planning

✔ Example: managing portfolio on apps like Fidelity

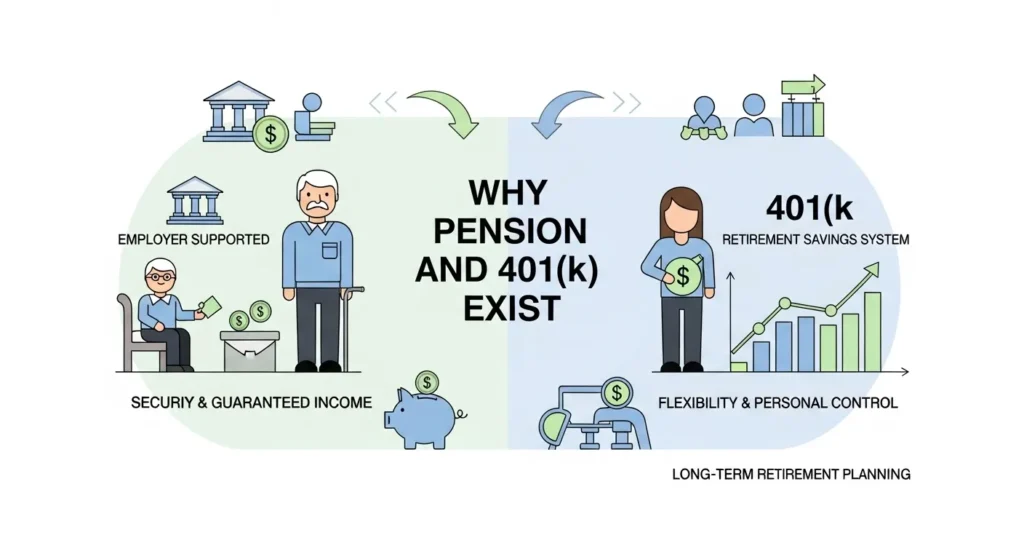

Why Pension and 401k Exist

The difference between pension and 401k exists because companies and governments created different systems to support retirement needs:

✔ Pension = traditional employer security system

✔ 401k = modern personal investment system

Platforms like Google Finance, Bloomberg, YouTube finance educators, and Meta business pages explain these systems for financial awareness and retirement planning.

WHEN TO USE PENSION

Use pension if:

✔ You want guaranteed income

✔ You prefer low risk

✔ You work in government or long-term companies

WHEN TO USE 401k

Use 401k if:

✔ You want investment growth

✔ You change jobs frequently

✔ You understand financial markets

WHY PEOPLE GET CONFUSED

✔ Both are retirement plans

✔ Both involve money saving

✔ Employer contributions overlap

✔ Financial terms sound complex

That’s why the difference between pension and 401k is heavily searched on Google.

Real Life Examples

Job Scenario:

- Teacher with pension plan

- Tech worker with 401k account

Retirement Planning:

- Pension gives fixed monthly income

- 401k depends on stock investments

Business Context:

- Companies offer pension for loyalty

- Startups offer 401k benefits

Financial Apps:

- Fidelity, Vanguard manage 401k

- Government systems manage pensions

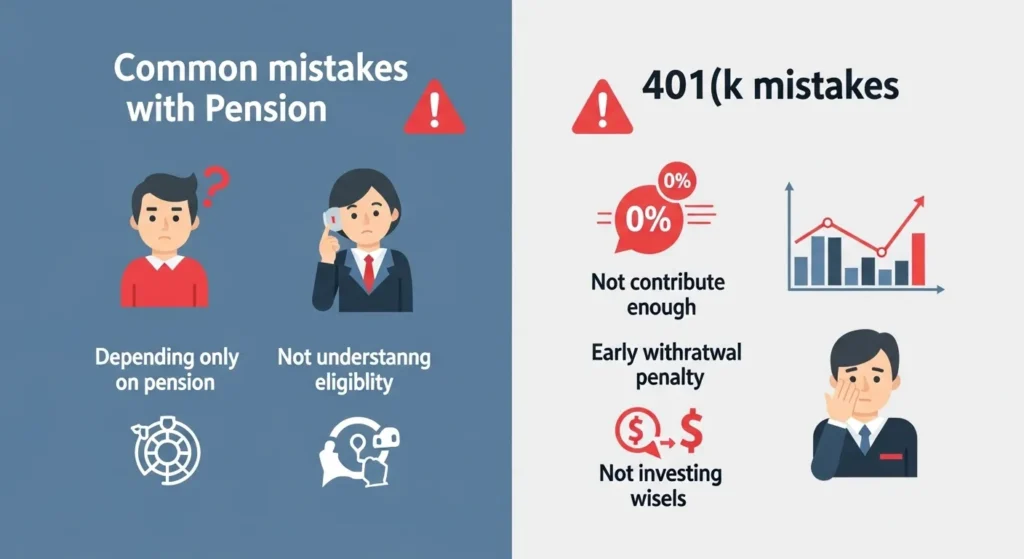

Common Mistakes with Pension and 401k

- Thinking both are the same

- Not understanding investment risk

- Ignoring employer contributions

- Withdrawing 401k early

- Not planning retirement early

✔ Fix: Learn both systems before choosing jobs

How Search Engines Understand This Topic

Google analyzes:

✔ Financial intent queries

✔ Retirement planning behavior

✔ Investment comparison searches

✔ User job-related intent

Platforms like LinkedIn, Google Finance, YouTube financial educators, and Meta career groups boost visibility of such content.

Expert Insight

From a financial planning perspective, the difference between pension and 401k reflects two retirement philosophies: security vs flexibility. In real financial advisory practice, pensions are considered stable but less flexible, while 401k accounts provide higher growth potential but require financial knowledge.

Most financial experts recommend combining both (if available) for balanced retirement security.

FAQs

1. What is the main difference between pension and 401k?

Pension is guaranteed income, 401k is investment-based.

2. Which is better, pension or 401k?

It depends on risk preference.

3. Can I have both pension and 401k?

Yes, in some jobs.

4. Is 401k risky?

Yes, it depends on market.

5. Is pension guaranteed?

Yes, usually fixed income.

6. Who manages pension?

Employer or government.

7. Who manages 401k?

Employee controls it.

8. Can I lose pension?

Rare, but depends on company stability.

Conclusion

The difference between pension and 401k is very important for understanding retirement planning. A pension is a traditional system where employers guarantee a fixed income after retirement, providing financial security and stability. On the other hand, a 401k is a modern retirement savings plan where employees invest their own money, giving them flexibility and potential for higher returns.

Many people confuse both systems because they serve the same purpose retirement income but work in completely different ways. Understanding the difference between pension and 401k helps individuals choose better jobs, plan savings wisely, and prepare for financial security in the future.

In simple terms, pension is about guaranteed stability, while 401k is about personal control and investment growth. Knowing this difference can significantly improve your long-term financial decisions and retirement lifestyle.

Read more about!

Difference Between Lamb and Goat: Easy Guide

I am Emily Johnson, a USA-based content writer who creates easy-to-read blogs on language and daily life topics. I explain complex ideas in simple English for students and beginners so they can understand easily.